Introduction

The Sugar and Alcohol Industries in Mexico have a long tradition and have therefore become one of the nation's leading agro-industries, currently cultivating approximately 650 thousand hectares of sugar cane; the sector has unlimited possibilities for use, both in terms of energy and industry.

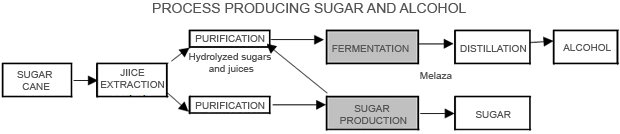

A major industrial use of sugar is the production of ethyl alcohol, which is obtained from the transformation of molasses as a raw material, reaching annual production figures exceeding 100 million liters of 96 º GL alcohol with yields of up to 250 liters of alcohol per ton of molasses.

The options for obtaining alcohol from sugar cane are as follows:

- Through the use of molasses;

- Using hydrolyzed sugars "A" and "B" with significant increases in yields and quality alcoholic beverages;

- Employing the sugar cane juice or "garapa" directly for this purpose: This takes place in distilleries and is dispensed from the sugar production area;

- Use of "low quality" juice (macerated and filtered)

Production

The production of alcohol has recently faced several restrictions; the following being the most important:

- High taxes;

- Sudden fluctuations in the price of hydrolyzed sugars in domestic and export markets;

- Environmental contamination by removal of stillage;

- Imports of ethyl alcohol with different tariff codes (lower taxes); and

- The use of backward fermentation technology.

Although several programs have been implemented to promote the expansion of the alcohol industry it has been influenced by other factors associated with the price of raw material and the currently shrinking supply of ethyl alcohol as well as the economic recession.

The recession experienced by the sugar industry has meant that only half of the distilleries that were operating in the late eighties are still operating today (harvest 2001/2002), only 16 in total. The refineries that have distilleries currently in operation are:

- Aarón Sáenz

- Calipam

- Constancia

- El Carmen

- El Mante

- El Potrero

- Emiliano Zapata

- Independencia

- La Joya

- La Providencia

- Pujiltic

- San Cristóbal

- San Nicolás

- San Pedro

- San Sebastián

- Tamazula

Cane alcohol production during 1990-2001reported an average annual growth of -0.39%; in that period the largest drop occurred in 1994 when production decreased by 13.52% while the largest increase was observed in 2000 with an annual growth of 19.21% (see table 1 in annex).

In 1990 62 million 365.4 thousand liters of alcohol were produced and in 1992 alcohol production rose to 70 million 991,700 liters, the highest of the decade.Thereafter production began to decline until 1996 when it fell to 49 million 82,600 liters. Later the industry began to pick up slowly, increasing production to 61 million 626.1 thousand liters in 2001 but still not exceeding the amounts observed at the beginning of the decade.

Apparent consumption (production + imports - exports) in the period 1990 to 2001 showed an average annual growth of 23.12%; in that period the largest drop occurred in 1998 when indicatorsreported an annual decline of -69.75%, while the largest increase was observed in 1999 with an annual growth of 204.55%. The largest apparent consumption in absolute terms was in 2001 reaching 200.7 million liters (see table 2 in annex).

Foreign Trade

Exports

Despite the trend to lower cane alcohol production in the last ten years, the export of alcohol from 1990-2001 registered an average annual growth of 19.02%. In 1990 it exported 22.5 million liters and in 1998 saw the greatest export of the period, 98.8 million liters.In 2001 exports of cane alcohol were estimated at 24.8 million liters.

In 2000 Mexico exported 63.1 million liters of ethyl alcohol destined mainly for the United States accounting for 77.0% of the total and 13.9% to Canada (see Table 3 in Annex).

Imports

In turn, imports of cane alcohol have shown rapid growth, from 47.9 million liters in 1990 to 164.0 million liters in 2001, while in the month of October 2002 these imports had already reached a level of 165.7 million liters (see table 2 in annex).

Imports of cane alcohol to Mexico in 2000 amounted to 127.2 million liters, mainly from the United States with 53.4% of total imports for that year; Brazil 16.8% and Guatemala 14.0% (see Table Annex 4). Cane Alcohol in the context of the Free Trade Agreement (NAFTA)

NAFTA was the first commercial treaty in the world that joined the single market (free trade zone) of two developed countries with a developing nation.This lead to negotiations of the Agriculture Chapter turning out asymmetrical and radicalas it included the entire agricultural and agroindustrial trade between the Contracting Parties without distinction, that is, no product was excluded from the Treaty and in the case of Mexico the protection margins for agricultural goods were far below international standards.

The resolutions adopted under NAFTA in the agricultural sector are included in Chapter VII and cover the following topics:

- Subsidies or domestic support

- Sanitary and Phytosanitary Measures

- Trading Orders

- Market Access

- Regulations of Origin

The trade provisions included in the first three items were established at the tri-national level, while those corresponding to Market Access and Trade Orders were negotiated bilaterally.

Subsidies or domestic support. (Article 704 of NAFTA)

In terms of domestic subsidies, NAFTA recognizes the lesser degree of development compared to Mexico's trading partners, therefore allowing the possibility of granting subsidies subject to reduction commitments in the negotiations under the World Trade Organization (WTO), such as non-exempt direct payments linked to production and prices and input subsidies needed to offset the subsidies granted by the U.S. and Canadian agricultural products considered highly sensitive. The support levels that were granted in Mexico before the entry into force of NAFTA were measured by the Aggregate Measurement of Support (AMS), however within the commitments made by Mexico under NAFTA, the replacement of its system of commercial price protection support for a system of direct payments was established.

The change of implicit subsidies in the guaranteed price system for the system of direct payments to producers led to programs such as "PROCAMPO".

Export subsidies (Article 705 of NAFTA)

The main agreement in this regard was the commitment of the Parties to gradually eliminate subsidies in agricultural trade. Mexico may import subsidized products from the U.S. or Canada, or countries outside the free trade zone, provided it does not affect the agricultural exports of the other two NAFTA partners.

For the particular case of the United States and Canada, export subsidies of agricultural products to the Mexican market are allowed but only to counter subsidized exports from other countries, while between the U.S. and Canada the use of direct export subsidies when products are destined for their marketsis prohibited.

Sanitary and Phytosanitary Measures (Chapter VII, Section B of NAFTA)

In NAFTA rights and obligations were established on sanitary issues for the three parties, determining the equivalency principle by which various measures are considered identical in terms of risk. It stipulates the obligation of the Parties to use the dispute settlement mechanism established under NAFTA or go to international or regional organizations such as the WTO for consultation and recommendations.

Likewise, it was agreed to declare areas of low pest prevalence or pest free areas by region, which benefit some Mexican farmers by allowing them to increase their exports and not subject their entire production to obstacles imposed by the United States because of the presence of some pests.

Trading Orders (Annex 703 of NAFTA)

Norms and Quality Standards such as trading orders were regulated in the Treaty and it was determined that normative measures or trading applied to domestic products be the same as those applied to the goods of another Party where they are intended for processing.

Market Access (Article 703. Section A of NAFTA)

In NAFTA, measures and procedures from the GATT were adopted in terms of market access and safeguards, although with greater speed and liberalization.

Tariffs. - In the NAFTA the Parties agreed to eliminate all theirnegotiated tariffs over a period of 15 years from its entry into force on January 1, 1994, i.e. on January 1, 2008 all goods shall be tax exempt in the three countries. In this regard, five categories of tax relief were established:

Category A: Includes goods whose tariffs were fully paid up prior to the entry into force of the Treaty.

Category B: These goods will be fully tax exempt within 5 years, i.e. from January 1, 1994 to January 1, 1998; those goods considered very sensitive for their immediate liberalization were included in this category.

Category C: This category included products to be fully tax exempt over a period of 10 years, from January 1, 1994 to January 1, 2003.Category C+: Includes goods that will be fully tax exempt over a period of 15 years and that are considered sensitive to importation. The United States placed select fruits, citrus fruits and some vegetables in this category while Mexico didn't place any products in this category.

Category D: All goods that were fully tax exempt from the date of entry into force of the Treaty were included, i.e. on January 1, 1994. Transition Category C (Tariff Quota): This category included sensitive and extremely sensitive agricultural products that would be tax exempt within a period of 10 to 15 years under a tariff-quota system that provides additional protection.

In this category Mexico included goods with prior import license before the entry into force of the Treaty. Within the goods considered sensitive and tax exempt within a period of 10 years, pork products, apples and potatoes were included, while in those goods considered extremely sensitive to tax exemption over a period of 15 years, Mexico included imports from U.S. such as corn, beans and powdered milk, while U.S. imports from Mexico included sugar, peanuts, orange juice concentrate, frozen and non-concentrated orange juice.

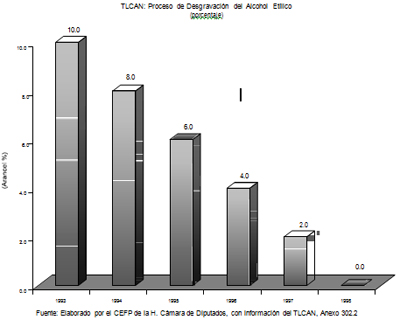

It is worth noting that in Article 302 of NAFTA on tariff reduction it was agreed that, upon request and agreement of the parties, the tariff reduction process could be accelerated faster than originally agreed, without the need to renegotiate this agreement or reopen the case.

Tariff Reduction Process for Sugarcane Alcohol

For the particular case of alcohol from sugarcane, in the NAFTA Mexico agreed to deduct the fraction 22.07.20.01 (Ethyl alcohol and other spirits, denatured, of any strength) for imports from the United States in a linear term of 5 years, i.e. this fraction was completely tax exempt from January 1, 1998 (see chart below), while the fraction 22.07.10.01 (Non-denatured ethyl alcohol of alcoholic strength exceeding or equal to 80% vol.) was completely released before the entry into force of NAFTA, therefore the United States and Canada can freely export this type of alcohol to Mexico. In general, the agreement for tariff reduction of ethyl alcohol under the NAFTA to the List of Tariff Reduction Items submitted by Mexico was as follows:

For the particular case of alcohol from sugarcane, in the NAFTA Mexico agreed to deduct the fraction 22.07.20.01 (Ethyl alcohol and other spirits, denatured, of any strength) for imports from the United States in a linear term of 5 years, i.e. this fraction was completely tax exempt from January 1, 1998 (see chart below), while the fraction 22.07.10.01 (Non-denatured ethyl alcohol of alcoholic strength exceeding or equal to 80% vol.) was completely released before the entry into force of NAFTA, therefore the United States and Canada can freely export this type of alcohol to Mexico. In general, the agreement for tariff reduction of ethyl alcohol under the NAFTA to the List of Tariff Reduction Items submitted by Mexico was as follows:

Conclusions

- Despite the ups and downs faced by the alcohol industry in Mexico, it still holds an important position in the agroindustrial sector, currently cultivating over 650 hectares of sugar cane where the raw material for the manufacture of ethyl alcohol is extracted from, which has a wide variety of industrial and energy based uses.

- The production of ethyl alcohol in Mexico has maintained an essentially down ward trend in the last ten years, while demand has grown considerably; therefore increasing amounts of alcohol from the United States have had to be imported. This situation is further aggravated by the economic recession facing the country and other factors associated with the price of raw materials (sugar molasses).

- Trade liberalization has played an important role in the growth on imports reported in the last five years, particularly the agreements adopted by the Free Trade in North America which allowed Mexico to fully eliminate tariffs. Even before this Treaty entered into force, the fraction 22.07.10.01 (Non-denatured ethyl alcohol of an alcoholic strength of not less than 80% vol.), while the fraction 22.07.20.01 (ethyl alcohol and other spirits, denatured, of any strength) was completely tax exempt within a period of five years from the entry into force of the Treaty,i.e. the fraction was completely deregulated for imports from the United States as of January 1, 1998.